Restoration: margin and ratio calculation

Quels sont les indicateurs de performance en restauration, quel est le calcul marge restaurant, comment définir le prix de ventes d’un plat, comment utiliser le coefficient multiplicateur en restauration ? Voici quelques une des questions qui nous sont régulièrement posées. Nous allons donc dans cet article distinguer les différents indicateurs utilisés en restauration. Ces indicateurs de performances permettent au gérant de contrôler la gestion globale de son restaurant, de maintenir l’équilibre et de s’assurer de la santé financière de son établissement.

Le taux de marge brute est un indicateur clé. En effet, il permet de fixer le prix de vente des produits de votre entreprise commerciale. Il est donc primordial d’optimiser au mieux ce taux. Cela passe en particulier par le prix des achats de matière première et des marchandises qui servent à votre production.

Free Trial | Koust Application

Indicateur principal de Calcul marge restaurant

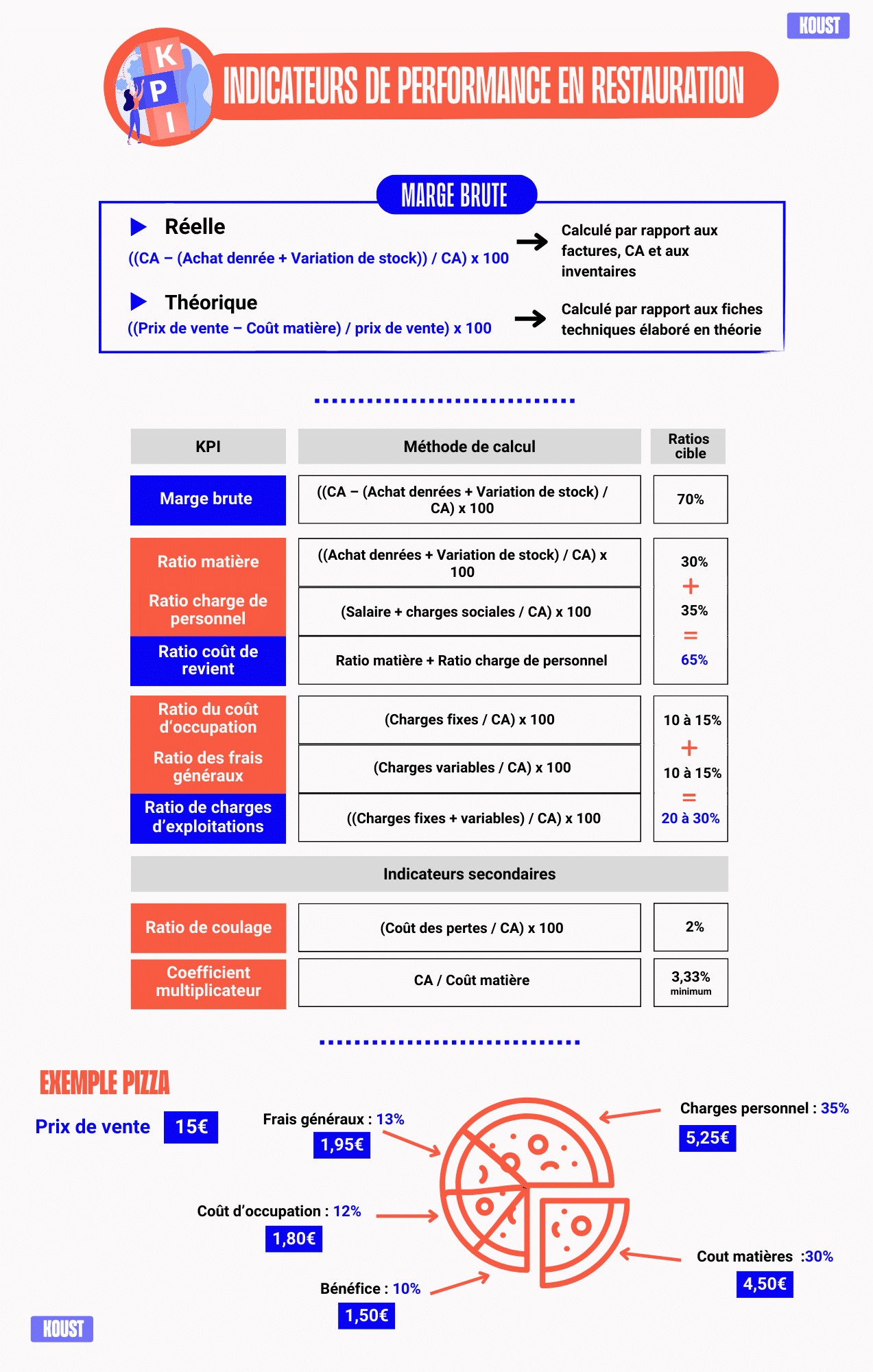

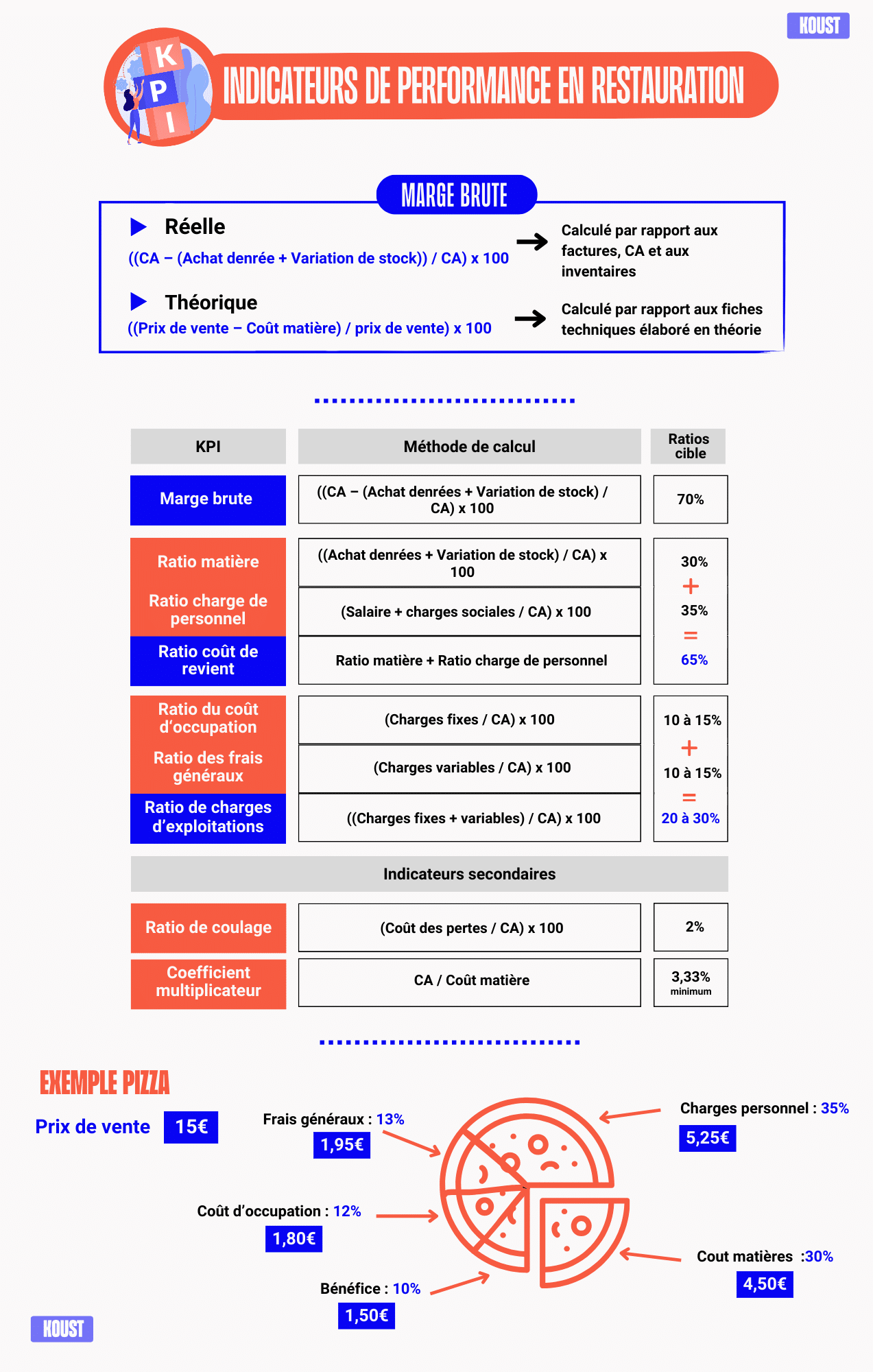

Gross margin

Pour une activité comme la restauration, le premier indicateur de performance analysé est la marge brute.

Elles n’est autre que le chiffre d’affaires réalisé auquel l’on a soustrait le coût des matières premières. Le calcul de la marge brute se fait de façon théorique, lors de la création d’un plat ou de façon réel sur une période définie.

Dans ce deuxième cas, le calcul marge brute ce fait au niveau global du restaurant ou sur l’un des pôles d’activités (bar, cuisine, snack…) à condition d’avoir isolé les ventes ainsi que les achats de matières premières.

The gross margin generated must make it possible to cover all costs (excluding material costs) while generating a profit.

Aclear distinction must be made between the theoretical gross margin and the actual gross margin.

Calculation of the theoretical gross margin

It is done on the data sheets, usually for a portion.

Lors de la création d’un restaurant ou d’une nouvelle carte, on anticipe le coût des matières premières via les fiches techniques (théorie). Ce sont des prévisions qui ne tiennent pas compte de la qualité de la gestion de stock. Les ingrédients sensibles (fragile et/ou chère) sont sujets à la perte (DLC dépassé, proportions mal respectées, vol, casse, etc.). Autant de facteurs qui altèrent la performance de la marge brute réelle.

Theoretical gross margin calculation = ((Selling price - Material cost) / selling price) x 100

Actual gross margin calculation

Il s’effectue sur une période définie (jours, mois, année…). Elle prend en compte les achats, la variation de stock, les ventes réelles, ainsi que les pertes, casses et offerts altérant vos prévisions théoriques.

Calculation of actual gross margin = ((Sales - (Purchased goods + Inventory change)) / Sales) x 100

Analysis of the results

La marge brute doit être régulièrement analysée (par jour, mois, trimestre, année, etc.) ainsi que par secteur (bar, cuisine, snack, etc.).

What is its evolution? Is it decreasing? Your short and medium-term strategy is based on the reflections of this analysis. Identifying poor performances and their origins allows you to implement relevant corrective actions.

Renegotiating your purchase prices with your suppliers, reviewing the composition of your recipes, improving your inventory management or strengthening your leading products are all corrective actions that together improve your gross margin.

The ratios used

Material ratio (Food cost)

Le ratio matière (Food Cost en anglais) est tout simplement le coût des matières premières utilisées, exprimé en % du CA.

It makes it possible to check the importance of the material cost in relation to the turnover achieved.

Tout comme la marge brute, il se calcule en théorie sur la fiche technique, et en réel sur une période définie.

Généralement, un ratio matière cible est fixé par la direction. Le chef de cuisine a pour objectif de le respecter. Un ratio matière trop élevé va forcément diminuer la marge brute au risque de voir l’équilibre financier du restaurant altéré.

Material ratio = ((Material cost + Inventory change) / Sales) x 100

* Inventory change = Beginning of period stock - End of period stock

Margin calculation: Labor cost ratio

Le ratio de charge de personnel représente le % du CA alloué aux salaires et charges sociales.

Le coût de la main d’œuvre est élevé en restauration, il représente en moyenne entre 35 % et 40 % du CA.

Personnel expense ratio = (Labour cost/sales) x 100

Prime cost ratio (Prime cost)

The cost ratio is a ratio specific to the restaurant industry. It is equal to the sum of the material ratio and the staff cost ratio.

Ce ratio représente donc le % du CA alloué à la réalisation des plats (coût matière + personnel). Il doit ce situé au alentour des 65 % du CA.

Costing Ratio = Material Ratio + Personnel Expense Ratio

More information about the cost of return here: https: //koust.net/calcul-cout-revient-restauration/

Margin calculation: Occupancy cost ratio

Le coût d’occupation est composé uniquement des charges fixes (loyers et charges locatives, emprunts…). Il constitue à peu près 10 % à 15 % du CA.

Occupancy Cost Ratio = (Fixed Charge / Sales) x 100

Overhead ratio

Vos frais généraux sont composés de vos charges variables (gaz, électricité, impôts et taxes, commission sur les moyens les paiement, personnel extérieur, publicité…). Il avoisine les 10 % à 15 % du CA.

Overhead Ratio = (Overhead / Sales) x 100

Operating expense ratio

Le Ratio de charges d’exploitation représente le % du CA alloué aux charges fixes et variables du restaurant. Il est le cumule du coût d’occupation et des frais généraux. Il se situe autour de 25 % à 30 % du CA.

Operating expense ratio = ((Fixed expenses + Variable expenses) / Sales) x 100

Casting ratio

The leakage ratio corresponds to the impact of losses (breakage, expired product, theft...) on your turnover.

Pour pouvoir le calculer, il faut peser les pertes et les renseigner (logiciel de gestion, Excel…) afin d’en calculer le coût. Attention, ce ratio est très important et parfois difficile à quantifier. Il ne doit pas dépasser les 2 % du CA

Casting ratio = (Cost of losses / Sales) x 100

Summary of ratios used in restoration

Monthly monitoring of ratios is essential in order to check the proper control of costs. This allows us to quickly identify areas for improvement as well as the corrective actions to be taken.

| Performance indicator | Calculation method | Target ratio |

| Gross Margin | ((Sales - (Purchase of goods + Change in inventory) / Sales) x 100 | 70% |

| Material ratio (Food Cost) | ((Purchase of goods + Change in inventory) / Turnover) x 100 | 30% |

| Labor Cost Ratio | (Salary + social security charges / turnover) x 100 | 35% |

| Prime Cost Ratio (Prime Cost) | Material ratio + Personnel expense ratio | 65% |

| Occupancy cost ratio | (Fixed charges / CA) x 100 | 10 à 15% |

| Overhead ratio | (Variable expenses / CA) x 100 | 10 à 15% |

| Operating expense ratio | ((Fixed + variable costs) / CA) x 100 | 25 à 30% |

| Casting ratio | (Cost of losses / CA) x 100 | 2% |

| Multiplier coefficient (solid) | CA / Material cost | 3.33 min |

{kind=link}

Other indicators Margin calculation: The multiplier

The multiplying coefficient is a tool that makes it possible to define the selling price of a dish according to its material cost (example 1). It is sometimes used as a performance indicator by calculating it for all of the restaurant's services (example 2).

The multiplying coefficient is equal to the ratio between your "Selling price excluding VAT" and your "Cost of materials".

Pour un ratio matière de 30 % sur les solides, le coefficient multiplicateur est de 3,33. Pour les liquides, il peut être très variable, en moyenne, il se situe au alentour de 4 à 6.

Example 1:

You wish to offer a dish of Osso Bucco to your customers, you know your material cost and are looking to define your selling price including all taxes.

Votre plat vous coute 3 € HT en matière première par portion.

La TVA de vente est de 10 %.

Le coefficient multiplicateur moyen en restauration est de : 3,33.

Donc : (Coût matière x coef multiplicateur) x TVA = Prix de vente TTC

Donc : (3 € x 3,33) x 1,10 = 11 € TTC

Vous pouvez proposer votre plat au prix de 11 € TTC afin de pouvoir couvrir l’ensemble de vos frais avec la marge brute généré.

Example 2:

You wish to analyze your average multiplier coefficient realized over the year n-1

Le calcul est le suivant : CA / Cout matière = Coefficient multiplicateur moyen de l’année n-1.

Tout comme la marge brute, il est idéal de contrôler le coefficient multiplicateur moyen réalisé par période et, si possible, par pôle d’activité.

The average ticket

Le ticket moyen est l’addition moyenne de votre clientèle. Il se calcule par jour, semaine, mois, année… Il est le rapport entre votre CA et votre nombre de clients. Un ticket moyen en hausse signifie que votre clientèle ne consomme plus ou des produits chers. Il est un bon indicateur du budget moyen de votre clientèle ou encore, de la performance de vente de votre équipe.

Average ticket = Turnover incl. VAT / Number of customers

Conclusion margin calculation

Nombre d’indicateurs de performances sont utilisés en restauration. Leur but est de vérifier le bon équilibre financier du restaurant. Ils permettent d’identifier la source de dépense trop lourde afin d’en déterminer l’origine et de mener à bien des actions correctives ciblées. Un contrôle mensuel des ratios est donc essentiel.

Free Trial | Koust Application

For more information, please contact us.